Spray Foam Insulation: A Look Into Mortgage Issues

Spray foam insulation is a widely used and effective technique for insulating homes. However, it has become a contentious issue in the mortgage industry, as it can potentially complicate securing a mortgage for properties that have it installed. With over 250,000 homes in the UK featuring spray foam insulation, this issue has become a pressing concern for secured lending. At Countrywide Coatings, we recognise the significance of this issue and endeavour to provide comprehensive guidance on its complexities.

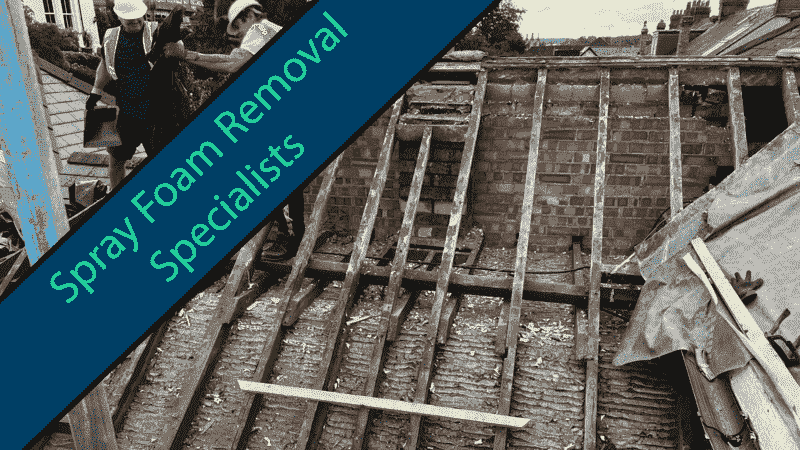

Spray foam insulation, or spray polyurethane foam, is an alternative insulation method to conventional types such as mineral fibre rolls or fibreglass wool. It is applied using spray guns in a liquid state and solidifies into a robust coating. Its fluid form permits simple usage in various areas, such as floors, walls, lofts, or roofs. However, the primary challenge in mortgage lending arises when applied to a property's roof space.

Two primary types of spray foam insulation are available: open-cell and closed-cell. Open-cell foam provides a more flexible and spongy material, whereas closed-cell foam has a sealed cell structure, providing a more stable and firmer end product.

Homeowners often choose Spray Foam insulation due to its insulating properties, which promise to reduce energy bills. Government grants also incentivise homeowners to invest in energy-efficient improvements, increasing the use of spray foam insulation in recent years. However, it is crucial to be aware of the long-term issues associated with it.

Spray foam insulation poses a problem for mortgage lenders as many decline properties with spray foam insulation due to potential issues, whether a residential mortgage or an equity release product. SPF insulation can restrict air circulation, leading to condensation and potentially damaging roof timbers. Closed-cell foam insulation, in particular, can harden excessively, stressing supporting timbers and distorting the roof structure. Its liquid form makes removal challenging and costly, often exceeding the original installation cost. Moreover, removing it might require replacing the entire roof if sprayed directly onto the tiles.

At Countrywide Coatings, we prioritise addressing these issues. While our Classic range of lifetime mortgages considers spraying foam insulation under specific conditions, including BBA approval and adherence to building regulations, advisers must manage client expectations. Currently, most lenders reject properties with spray foam insulation except under stringent conditions.

Advisers must inform clients of the consequences of installing spray foam insulation after completing their lifetime mortgage. It violates mortgage terms and adversely affects property resale value, potentially compromising clients' ability to fund their retirement.

In conclusion, spray foam insulation, which appears to be a straightforward solution, presents complex challenges in the mortgage industry. At Countrywide Coatings, we strive to navigate these complexities, providing informed guidance to advisers and clients.

Other Areas We Operate In

By accepting you will be accessing a service provided by a third-party external to https://countrywidecoatings.co.uk/